Public debt can be defined as the total sum of money owed by the national government to its creditors. Public debt is either domestic, external (foreign) or guaranteed. Domestic and external debt refers to financing obtained locally and internationally respectively while guaranteed debt is security offered by the Government to lenders should a counterparty default in its obligations. According to data from The Quarterly Economic and Budget Survey 2019/20, Kenya’s total debt stood at Ksh 6.7 trillion shillings as at the end of June 2020 which is equivalent to about 66% of total national wealth.

Government expenditure is split into two categories namely recurrent and development expenditure. Ordinarily, recurrent expenditure is mostly financed by tax revenue while development expenditure is financed by a hybrid model consisting of tax revenues and debt. In the past decade, as part of its development agenda, the Kenyan Government has commissioned large infrastructure projects such as the Standard Gauge Railway, the Lappset corridor and the expansion of various road networks, which aim to facilitate quick and efficient movement of people and goods hence spurring economic growth. These projects have been financed greatly by debt from multi and bilateral lenders. In addition, unexpected events such as the locust invasion, floods and the COVID-19 pandemic have forced the Government to seek additional financial assistance both locally and internationally.

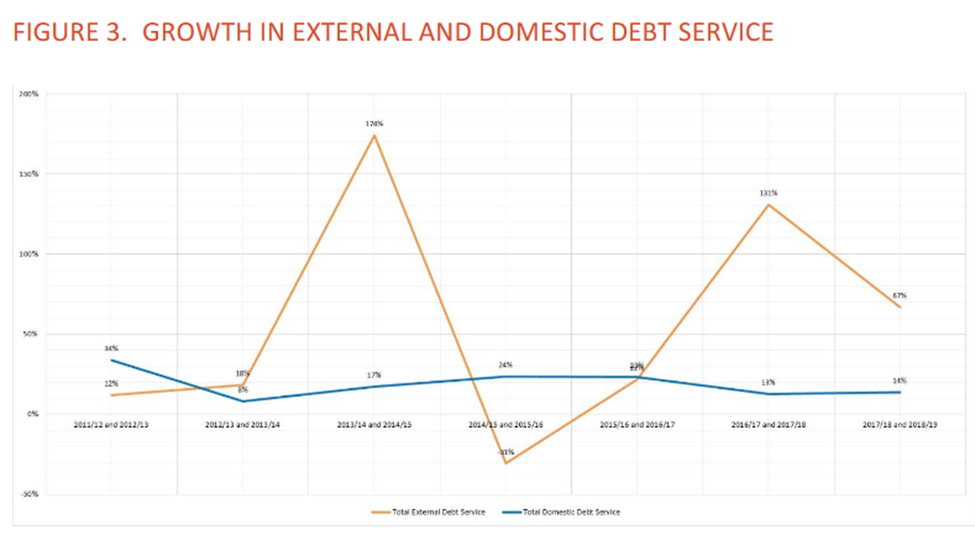

Although investing in such projects is key to enhancing economic growth, institutions such as the International Monetary Fund, the World Bank, the International Budget Partnership and rating agencies such as Moody and Fitch have flagged Kenya’s debt sustainability levels and expressed concerns that debt repayment obligations are getting more strenuous. In addition, Parliament’s approval to allow the Treasury to adjust the debt ceiling to Ksh.9 trillion thereby allowing the ministry to borrow more will compound the public debt problem in the long- run. Concisely figure 3 illustrates the trend in external and domestic public debt from 2017/18 to 2018/19.

Source: Annual Public Debt Reports 2017/18 and 2018/19

Insurance companies are large investors and have a long-term investment horizon compared to other players in the financial market. They help the system grow as they encourage stability through mitigation of risks and mobilization of savings. Insurance companies offer products that mandate them to provide returns to policyholders. These products mainly fall under life assurance and retirement benefits. In addition, in order to support their overall insurance business, insurance companies invest in various assets to boost their profitability thereby improving shareholder returns. However, the insurance industry investment strategy is guided by the Insurance Regulatory Authority (IRA) and Retirement Benefit Authorities (RBA). These agencies seek to protect policyholders by assessing the levels of asset exposure and providing guidelines on how to invest in various asset classes.

The different asset classes that insurance companies invest in both locally and internationally include Government securities, investment properties & REITS, ordinary shares and loans & mortgages. As at the end of the financial year 2019,the total value of the insurance industry investment portfolio stood at Ksh.590.67 Billion. As illustrated in the graph below, the insurance sector heavily invested in Government securities, real estate and ordinary shares which represented 61.5%, 14.2% and 9.2% of overall portfolio value respectively in 2019.

Source: Insurance Regulatory Authority 2019 Annual Report

By investing 61.5% of their portfolio value in government securities, the insurance industry is exposing itself greatly to opportunities and risks presented by this asset class. As the Government seeks additional financing to propel its agenda, it tends to attract potential lenders by offering attractive interest rates thereby positioning itself as a profitable and viable source of generating a return on investment. However, as debt levels grow, the ability of the Government to meet its repayment obligations diminishes and this creates a default risk thereby weakening the investment portfolios of investors. Although many economists have argued that Government’s default on local borrowing is low due to its ability to print money, this doesn’t provide any safety cushion since the relative value of the local currency will depreciate thereby negatively affecting portfolio value.

Based on IRA’s insurance industry investment guidelines, insurance companies are required to hold a substantial amount of their investments in ‘safe assets’ such as Government securities and balance the remaining amount across other assets classes. This greatly explains why insurance companies invested more than half of their portfolio in Government securities as earlier explained. With this in mind, the regulator has to assess the risk exposure in insurance portfolios and provide flexibility in investing in other asset classes thereby reducing the concentration risk in Government securities. To conclude, it’s important for all stakeholders to assess and evaluate trends in public debt and its ramifications both in the short and long term in insurance industry investment portfolios.

Article By Elizabeth Kamuu