Paragraph 10 of part II of the First Schedule of the Value Added Tax 2013 had exempted Insurance Agencies, insurance brokerage, stock exchange brokerage and tea and coffee brokerage services from VAT. This was meant to spur economic activity in sectors that had witnessed slow growth over the years. For example, by exempting VAT on insurance brokerage and agencies, the cost of purchasing insurance became low hence improving the overall insurance penetration (https://www.ira.go.ke/) rate from 2% in 2016 to 3% in 2019. However, the Tax Laws (Amendment) Act, 2020 mandates insurance brokers and agents to remit VAT on commissions received. This move will have ripple effects in the insurance industry considering that a substantial number of insurance policies in the Kenyan market are procured through agents and brokers. This article addresses the negative impact of this amendment to the insurance industry.

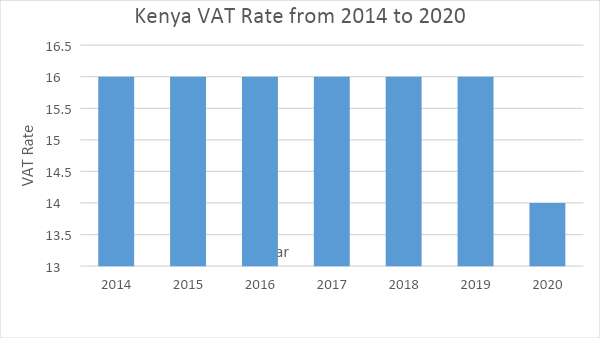

In Kenya, the sales tax rate is a charge to consumers based on the purchase price of certain goods and services. The graph below indicates that the rate was constant at 16% between 2014 and 2019. However, due to unexpected events both locally and globally, the Government opted to reduce the rate by 2 percentage points to 14% in 2020.

Graph 1: Sales tax rate (VAT)- Data from tradingeconomics.com

Following the adverse effects brought about by the COVID-19 pandemic and invasion of locusts and floods that led to concerns about food security, the displacement of people and the destruction of property and infrastructure, the Kenyan government came up with a rapid economic stimulus packages to help counter these effects. One of the measures that the Kenyan Government undertook was to reduce Value Added Tax from 16% to 14% as illustrated in graph 1. This was meant to trigger consumption in the economy as the Government anticipated depressed demand for goods and services as consumers were faced with difficult financial decisions during this period. It was clear that this move would affect Government tax collection targets hence necessitated the introduction of new taxes in areas that were exempted before. It is paramount to note that the tax structure in Kenya is skewed heavily towards income taxes and VAT.

It is assumed that prices of insurance products are arbitrarily fixed. Insurance intermediaries have argued that the introduction of VAT will push insurance premiums higher and force consumers to find other cost-effective ways of transferring risks. In addition, they claim that in the long run, the insurance market will contract and government’s tax collection will decline if this amendment is not retracted. Insurance premiums are generated after careful consideration of various personal and economic factors and supported by probabilistic actuarial models. Adding VAT complicates pricing models and transfers additional costs to the final consumer.

Needless to say, that the intermediaries are already paying withholding tax on the insurance products, and are now required to remit VAT on the same. That sounds like double taxation, don’t you think?

Marina et al. (2000) states that: The objective of a good tax system is to distort or alter as little as possible the economic decisions of persons and firms as compared with the decision they would have made if the taxes were not collected at all.” However, the action on the VAT amendment on Insurance agency and broker commission would unnecessarily complicate a relationship that is supposed to be simple and understood.

The Association of Kenya Insurers (AKI) opposed the amendment on the basis that their members will be mandated to collect and remit VAT on behalf of intermediaries who sell policies to the final consumer. Currently, insurance companies are required to deduct withholding tax from commissions paid to intermediaries and mandating them to additionally collect and remit VAT will not be cost effective. How would intermediaries take charge of VAT on the same product that has been subjected to withholding tax collected by insurance companies?

The Association of Kenya Insurers (AKI) was subsequently granted Conservatory Orders thereby suspending further implementation, administration, application and enforcement of the VAT amendment law. Consequently, members of AKI have been advised not to honor any tax invoices raised by partner intermediaries until the matter is determined on Tuesday, 3rd November 2020. This, therefore, means that the payment of commission has returned to the status quo ante. It is my hope that an amicable solution will be found between the insurance industry and the Government.

Written by: Elizabeth Kamuu